ROIC

- Jagannath Kshtriya

- Apr 1

- 2 min read

The creation of value is highly correlated with the efficient and effective use of capital. ROIC is vital to value creation, but many companies don’t focus enough on improving their ROIC.

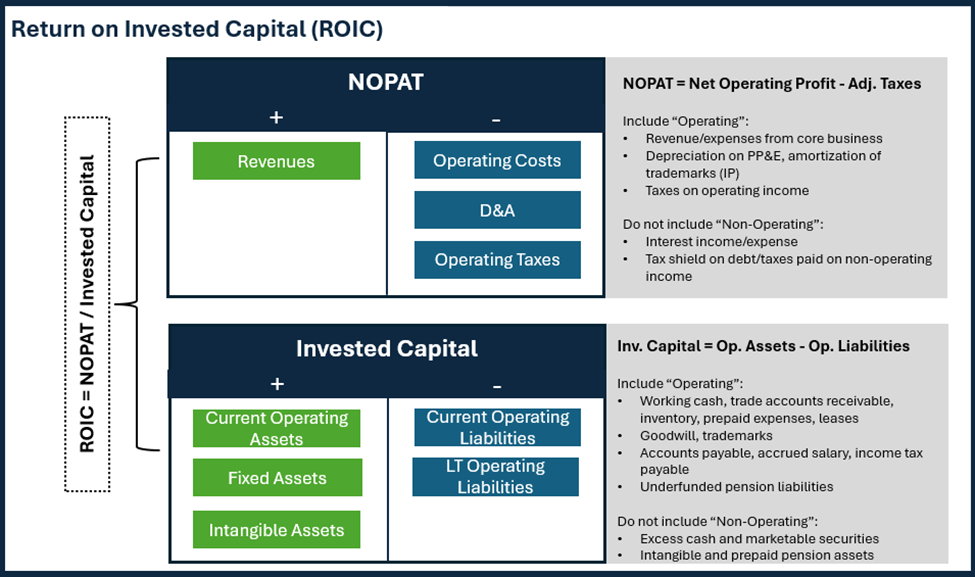

Return on invested capital (ROIC) is an important driver of corporate performance. It measures how much profit a company generates for every dollar invested in the company and helps in understanding the company’s economic returns.

ROIC is a strong driver of stock prices and equity valuation. Top-line growth and profit growth also help drive stock price, but ROIC is, by far, the most important driver because the market cares most about assigning value to the companies that produce the most cash per dollar of capital invested in them. If the opposite were true, the market would quickly go bankrupt. If you believe in any sort of efficiency in the stock market, ROIC is preeminent.

ROIC is meant to indicate how efficiently a company’s management team has allocated investors’ capital. It isn’t necessarily a fair way to compare companies across industries, because some industries are more capital intensive than others.

Digging further into ROIC, the carrying value of a company’s stock may be much lower than its current market capitalization. The company may have issued most of its shares many years ago at a price much lower than the current price. If a company has issued a relatively large amount of newer shares recently, or at high prices, its ROIC will be lower. If a company has low debt, its ROIC is higher. If a company is being forced to increase borrowings, especially when interest rates are high, its ROIC will go down.

For example, if a company raises money to acquire other companies, its capital will increase and its return on invested capital will go down. The acquiring company’s management team expects the new acquisitions will make it more profitable over the long term.

But if the company later writes down the value of the acquired assets, it may book a net loss at that time, which lowers its ROIC temporarily. But the accounting treatment is such that the invested capital that was written down is no longer included in ROIC calculations. Write-downs can boosts ROIC over time.

When something is written down, it disappears. There is a charge on the income statement at that time. What we do is take it out of the income statement and leave it as part of total invested capital.

The “proper definition” of invested capital is “all the capital that has been invested in a company over its lifetime”.

Comments